Historical Background

20 January 2004 – Signing of Executive Order 272 authorizing the creation of SHFC

21 June 2005 – Approval of SHFC registration to the Securities and Exchange Commission (SEC)

03 October 2005 – Appointment of Atty. Fermin T. Arzaga as the new SHFC President

24 October 2005 – SHFC Inauguration and First Board Meeting

03 November 2005 – Execution of Memorandum and Trust Agreements between NHMFC and SHFC

22 January 2007 – Transfer of SHFC to its corporate office at the Paseo de Roxas Avenue, Makati City

27 July 2007 – Creation of the Localized Community Mortgage Program (LCMP)

25 January 2011 – Appointment of Ms. Ma. Ana R. Oliveros as the new SHFC President

16 May 2011 – Approval of the Revised CMP Guidelines

17 May 2011 – Awarding of the first taken-out project under the LCMP (Sunrise HOA, IGAC

The SHFC

The Social Housing Finance Corporation (SHFC) was created through Executive Order No. 272 (E.O.272), which directs the transfer of the Community Mortgage Program (CMP), Abot Kaya Pabahay Fund (AKPF) Program, and other social housing powers and functions of the National Home Mortgage Finance Corporation to the SHFC.

Mandate

Under E.O. 272, the SHFC shall be the lead government agency to undertake social housing programs that will cater to the formal and informal sectors in the low-income bracket and shall take charge of developing and administering social housing program schemes, particularly the CMP and the AKPF Program (amortization support program and development financing program).

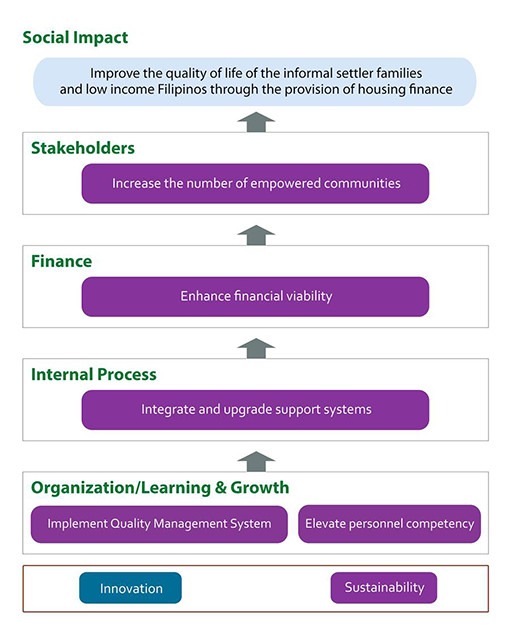

Our Vision

By 2040, SHFC is the lead key shelter agency implementing transformative and sustainable housing solutions towards inclusive growth and development.

Our Mission

SHFC empowers women and men to build Resilient, Inclusive, Sustainable, and Empowered (RISE) communities by providing Flexible, Affordable, Innovative, and Responsive (FAIR) housing solutions through strong partnerships with public and private stakeholders.

As a dedicated housing agency, we are committed to serving people with professionalism and managing resources prudently. We promote a culture of accountability and transparency, prioritizing the best interests of our communities and other stakeholders. We value our employees and ensure that the organization operates efficiently and effectively to fulfill its mandate.

We foster inclusive growth through accessible and community-driven housing solutions that significantly improve the quality of life.

OUR CORE VALUES

Service

Upholding the highest standards of conduct, proficiency, and ethical behavior as dedicated public servants.

Honor

Keeping high ethical standards at the corporate and individual levels, while setting and implementing performance standards that are clear and understandable to the public.

Fairness

Ensuring that everyone, regardless of gender identity, receives equal access, impartial treatment, and equal rights to safe, resilient, sustainable, affordable, and inclusive housing.

Competence

Exhibiting excellence in every endeavor through technology and innovation, while putting premium to sustainability and the proper use of internal resources.

THE BIRTH OF CMP

During the 1980s, unlawful occupancy of vacant lots were rampant in urban areas as residential space prices continued to rise beyond the reach of poor families. Land has become more limited due to higher urban population, increased construction of government infrastructures, and competing commercial use. These challenges resulted in evictions of families, pushing them to live precariously under extremely unhealthy conditions in the crevices of the cities such as waterways, railway tracks, foreshores, and even dumpsites.

Thus, the birth of CMP in 1988 came as a bright ray of hope for ISFs because it provided them with better access to affordable housing loans. The program was launched that year to give flesh to the social justice provision of the newly promulgated 1987 Constitution, Article XIII of which commands the State to undertake “a continuing program of urban land reform and housing which will make available at affordable cost, decent housing and basic services to under- privileged and homeless citizens.” CMP was intended to be an asset redistribution scheme where homeless low-income families could acquire land through affordable mortgage financing and hold it in the concept of community ownership. The program aimed to help the urban poor – mainly communities of informal settler families (ISFs) – acquire security of land tenure through the purchase of the land they had been living on, or the lots to where they shall be relocated to, and thereby share in the prosperity that the country was expected to generate after the People Power Revolution.

No one was to be left behind.

The concept of “community mortgage” was first introduced in Cebu by peoples’ organizations and community-based organizations in the early 1980s. When he was appointed commissioner of Presidential Commission for the Urban Poor (PCUP), Francisco Fernandez and like-minded advocates pushed for the institutionalization of the community mortgage program. Teodoro Katigbak, the chairperson of the Housing and Urban Development Coordinating Council (HUDCC) then, supported the proposal by creating an inter-agency committee composed of representatives from HUDCC, National Home Mortgage Finance Corporation (NHMFC), Home Guaranty Corporation, and the PCUP. This committee concluded after a thorough analysis that the existing Unified Home Lending Program (UHLP) was inaccessible to ISFs who were not members of either Government Service Insurance System (GSIS), Social Security System, or Pag-ibig Fund; hence, they pushed for the creation of CMP.

In August 1988, CMP was formally institutionalized under NHMFC by then President Corazon Aquino as the answer to the deprivation of the ISFs. Due to its exceptional performance – the poor were found capable and willing to repay their CMP loans – the program was formally adopted as the flagship program for socialized housing under the Urban Development and Housing Act of 1992. To encourage landowners to participate by selling their land to urban poor communities, the law provided the former additional incentives in the form of exemption from payment of capital gains tax. Although fully implemented and operational, stable source of funding came only after two years when Republic Act 7835 or the Comprehensive and Integral Shelter Financing Act of 1994 was enacted.

In 2004, halfway through the impementation of CMP, civil society organizations, policy-makers and other stakeholders clamored for the establishment of a new office that would solely focus on social housing finance and community development schmes for low-income groups such as CMP. According to them, placing CMP under a mere task force unit of the NHMFC did not give justice to the gravity of the need for affordable housing. Moreover, the NHMFC was primarily engaged in promoting secondary mortgage market for private sector housing, thus it did not have the proper mandate to administer CMP. Then President Gloria Macapagal Arroyo heeded the plea of CSOs by creating the Social Housing Finance Corporation (SHFC) as a separate entity by virtue of Executive Order 272. This EO transferred the stewardship of the CMP to the corporation in 2005.

SHFC now functions as a separate corporation registered with the Security and Exchange Commission with corporate flexibilities in operations such as adoption of policies that considers the limitations and capabilities of ISFs and sourcing of funds for the program. CMP has since grown by leaps and bounds under its new corporate administrator.